Investment, Power and Protein in sub-Saharan Africa:

- Introduction

- Background

- Research Methodology

- Sub-Saharan Africa’s Agricultural Investment Landscape

- Investor Visions

- National Subsidies and Global Market

- Conclusions

- Glossary

Suggested citation:

Brice, J., (2022) Investment, Power and Protein in sub-Saharan Africa. TABLE Reports. TABLE, University of Oxford, Swedish University of Agricultural Sciences and Wageningen University and Research. doi.org/10.56661/d8817170

Summary

- The ‘protein diversification’ vision was held by a small group of mission-driven venture capital funds based in Europe and North America and by African alternative protein manufacturers. This vision remains outside the financial mainstream and the volume of investment currently associated with it is likely extremely small.

- Interviewees who held this vision shared other the investors’ assumption that protein consumption would grow rapidly across sub-Saharan Africa over time. However, they believed that for environmental and ethical reasons this demand should be satisfied not through the expansion and/or intensification of animal protein production but through the introduction of alternative protein products into the region’s food system.

- These investors typically did not finance any form of animal protein production and invested exclusively in startup firms producing alternative proteins. There was also little evidence that they were financing the wider value chains which might support alternative protein manufacturers – e.g. farmers growing crops such as legumes or restaurants and retailers which might stock their products. Their investments therefore appeared to be concentrated in the financial and technology hubs of South Africa.

- Such investors believe that if alternative protein producers can sell their products at a price similar to or lower than that of animal products then many sub-Saharan African citizens may choose to augment their consumption of animal proteins with plant-based, in vitro, insect-based or fermented alternatives. They expect that their investments will enable alternative protein manufacturers to scale up production (and reduce production costs) sufficiently to make their products price competitive with animal proteins.

- These ‘vegan venture capitalists’ appear to be the only significant source of investment to which sub- Saharan African producers (or aspiring producers) of alternative protein products currently have access. Perhaps partly as a result, African producers of alternative proteins currently appear to be operating on a relatively small scale.

- The author found no evidence that these (or other) investors were actively financing the cultivation of protein crops such as beans and legumes for human consumption in sub-Saharan Africa. The only interviewees to discuss investing in such crops during interviews were impact and private equity investors with interests in animal feed production, some of whom had encouraged smallholder farmers to begin cultivating soy for use in animal feed.

Who?

The final investor vision identified during this project is held primarily by a small (and unusual) group of self- described mission-driven venture capital funds based in Europe and North America and by the African alternative protein manufacturers in which they invest. While this vision motivates and mobilises a highly distinct network of investors and protein production enterprises which displayed little overlap with those described above, it remains outside the financial mainstream and the volume of investment activity associated with it is likely to be extremely small. One DFI interviewed during this project is currently exploring the possibility of making equity investments in African companies producing plant-based protein products. However, it had not yet made any such investments and was not aware of any other DFIs with plans to invest in alternative proteins. This reluctance among DFIs to invest in plant proteins may partly reflect uncertainty about the impact of any dietary shift towards alternative proteins on the livelihoods of small-scale livestock producers and thus about its alignment with their development objectives.

“It’s a very important point on the inclusivity. We need to really work that out, because that alternate protein has to be (...) tied up with a robust agricultural hinterland which uses, whatever, a contract farming model, a hub and spoke model, with pockets of smallholders (...) that directly benefit from the raw material supply. And everything has to be done at scale, and at the lowest cost, to make it affordable because (...) it should be primarily target for the local populations.”

(Interview 19, DFI)

Because venture capitalists were the only investors actively financing this vision, funding for alternative protein startups was provided largely through equity investments. Interviewees noted that the equity investments which they provided to African alternative protein companies were significantly smaller in size than either the equity investments often provided to their counterparts in Europe and North America by venture capitalists or the loans available to larger animal protein producers from commercial banks.

Why?

While interviewees who held this vision shared other investors’ assumption that demand for protein would grow rapidly across sub-Saharan Africa over the coming decades, they believed firmly that this demand could not (and should not) be satisfied solely through the expansion of animal protein production.

“There is talk about, you know, protein deficiency in Africa. It cannot be covered with animal protein only, there has to be a mix, you know. There will be more animal protein, but it can’t just be done by animals. There has to be... probably insects, but plant protein is probably one of the cheaper ways (...) From an investor point of view, I think people see the opportunities. (...) Africa’s doubling its population, people will need to eat and the food cannot just come from animals.”

(Interview 04, alternative protein company founder)

These interviewees argued that it would be both ethically preferable and more environmentally sustainable if much of this expected future demand for protein were satisfied through alternative protein products. They were therefore investing in startup firms producing either plant-based meat and dairy alternatives or animal proteins produced through in vitro cultivation of animal cells and precision fermentation technologies. Like other venture capitalists, these investors expected to receive a competitive rate of financial return on their investments. However, they were unusual in that their decisions appeared to be motivated less by commercial considerations than by a desire to limit the expansion of livestock agriculture in sub-Saharan Africa through increasing the production and consumption of alternative protein products.

“We quickly knew that in the beginning, [the company] has to be vegan- friendly (...) there are these investors that really, particularly want to fund alternative proteins, you know? And they were most responsive (...) we have nine different investors and, I mean, with different sizes of tickets. Three of them are not really vegan investors, you know, but the other six are. (...) I think in total money also, most of it comes from them. Like, 80% comes from vegan investors.”

(Interview 04, alternative protein company founder)

These ethical and environmental goals appeared to be the main reason why these ‘vegan venture capitalists’ had chosen (unlike most of their peers) to invest in African food technology companies. The co-founder of one African startup producing plant-based meat highlighted that such companies tended to fall into a funding gap lying between two distinct groups of investors. African banks and private equity funds tended to refrain from investing in alternative protein companies because they regarded them as being excessively risky investments. Meanwhile, most of the European and North American venture capital and private equity funds which had financed alternative protein startups in their home markets tended (as discussed previously) to regard sub-Saharan Africa as an unacceptably risky location in which to invest. It therefore appeared that these ‘vegan venture capitalists’ were motivated to invest in African alternative protein startups because they regarded the transformation of diets and food systems in the world’s most rapidly growing markets for protein away from meat and dairy as being a sufficiently important normative goal to override the risk of financial loss.

These ‘vegan venture capitalists’ appear to be the only significant source of investment to which African producers (or aspiring producers) of alternative protein products currently have access. One interviewee considered this an important constraint on his firm’s growth potential because it restricted him to a narrow pool of potential investors, most of whom had only relatively small sums of capital available to invest (with each venture capitalist typically contributing a sum in the tens to the low hundreds of thousands of US dollars).

What and where?

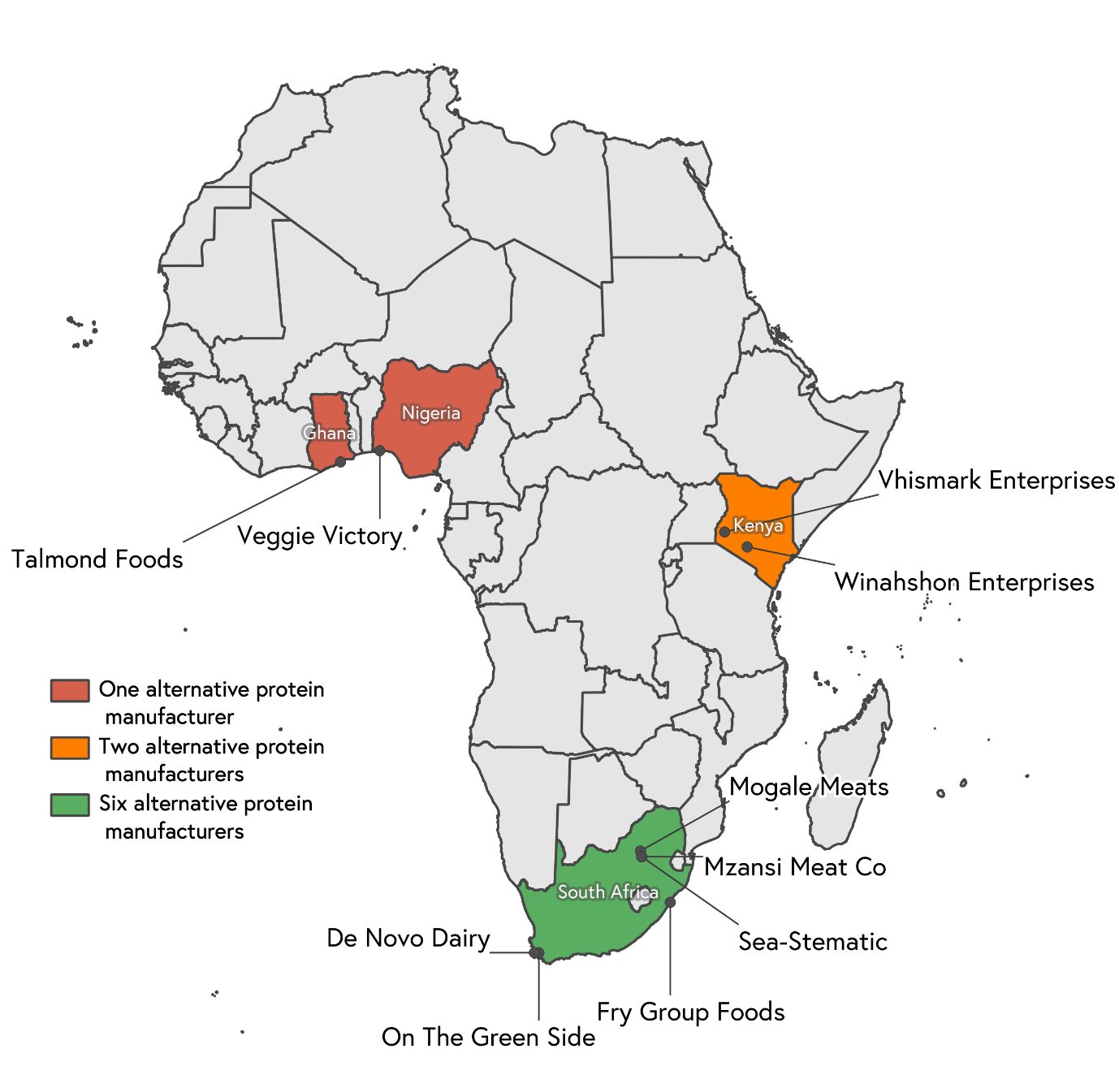

These investors typically did not finance any form of animal protein production (including aquaculture), and instead invested exclusively in startup firms producing alternative proteins. In order to assess the likely geographical focus of their investments, the author analysed the databases of alternative protein manufacturers maintained by the Good Food Institute and Crunchbase in order to establish how many such firms were active in sub-Saharan Africa and where they were headquartered(4). This analysis identified ten alternative protein producers as being active in sub-Saharan Africa. Six of these firms were located in South Africa, two were headquartered in Kenya, one was based in Nigeria and one was in Ghana. As such, it seems likely (as Fig. 14 illustrates) that investments made by these ‘vegan venture capitalists’ will display a high degree of geographical concentration around the financial and technology hubs of South Africa.

There was little evidence that this group of investors was actively financing other elements of the wider value chains which might support these alternative protein manufacturers – for instance farmers growing protein crops such as legumes or restaurants and retailers which might stock their products. Perhaps as a result, even African producers of more technologically proven alternative proteins such as plant-based meats currently appear to be operating on a relatively small scale and are predominantly targeting their products at urban consumers motivated by anxieties about health and food safety in relation to animal protein. One interviewee also noted that the fragmentation of the restaurant and food retail sectors in many sub-Saharan African counties – and their limited distribution infrastructures for chilled and frozen products – makes expansion into new regions and countries difficult and further constrains their ability to scale up production.

Figure 14: Map of alternative protein manufacturers within sub-Saharan Africa. Data source: Good Food Institute and Crunchbase.

How?

These investors’ theory of change could be summarised as follows. Adherents to the protein diversification vision expect population growth and economic expansion to drive a rapid increase in demand for protein in sub-Saharan Africa over the coming decades. While voluntary adoption of vegetarian and vegan diets is currently rare within the region, they believe that the environmental impacts of livestock agriculture mean that it will not be possible to satisfy future demand for protein sustainably by increasing production of animal products. They also observe that high rates of poverty mean that many people’s decisions about which foods to purchase and consume are acutely price-sensitive. As a result, these investors believe that if alternative protein producers can sell their products at a price similar to or lower than that of animal products then a substantial proportion of sub-Saharan African citizens may choose to augment their consumption of animal proteins with plant-based, in vitro, insect-based or fermented alternatives. They therefore hope that African consumers on constrained budgets might be persuaded to supplement their intake of animal products with price-competitive or cheaper alternative proteins.

“I strongly believe that the protein demand on this continent cannot just be covered by more livestock, it has to be a mix of several things, you know? Of course I wish it would be 100% plant-based, but that is utopia. But there will be more plant-based protein, probably also insect protein. I don’t know, maybe cultured meat. (...) So for me it’s going to be a mix and even if plant- based has, whatever, a 5% share, [that’s] good enough. Not good enough from an ideological point of view, but from a business point of view, that’s already huge.”

(Interview 04, alternative protein company founder)

Adherents to this vision expect that investment in alternative protein manufacturers will enable these companies to increase their scale of production (and to reduce production costs) sufficiently that their products become price competitive with animal proteins and secure a significant share of markets for protein in sub-Saharan Africa. This will enable investors in these firms to receive an attractive financial return on their investment, while also satisfying the region’s growing demand for protein and preventing the environmental damage associated with a large increase in livestock populations.

What about plant proteins?

Protein crops such as beans and legumes are consumed widely across sub-Saharan Africa, and are grown by many of the region’s smallholder farmers, and there is anecdotal evidence that some development funders are beginning to show interest in promoting the cultivation of soy for human consumption. However, the interviews conducted during this project found no evidence that adherents of the protein diversification vision (or indeed other investors) were actively financing the cultivation of these crops for human consumption.

Indeed, the only interviewees to discuss investing in such crops during interviews were impact and private equity investors with interests in animal feed production, some of whom had encouraged the smallholder farmers who served as their outgrowers to begin cultivating soy for use in animal feed production. One impact investor whose firm held equity investments in firms operating across several Southern and Eastern African countries highlighted that soy was neither part of a traditional part of local diets nor an established element of agricultural rotations in these locations. As such, local smallholders had only begun to cultivate soy after construction of a feed mill created a local market for this crop:

“So the quality of the feed that was available to the [poultry] farmers was really poor and particularly the protein content of the feed. Because nobody grew soya beans in Tanzania, pretty much, before we arrived (...) There’s virtually no commercial farms in Tanzania and these smallholders are producing maize, mono-cropping the maize. But we built a soya processing plant, which is the market for soya beans. (...) Then we reached out to some more of the farmers and said, “Why don’t you bring it into rotation for maize?” (...) soya’s good for smallholder farmers. It’s high value per tonne. You’re reducing disease pressures by stopping the mono-cropping. And you rotate the maize for the soya and then you’re fixing the nitrogen.”

(Interview 16, impact investor)

This interviewee was proud of the role that their investments in soy processing had played in creating a local animal feed industry. They highlighted that the cultivation of soy both returned nitrogen to the soil (reducing the need for smallholders to apply artificial fertilisers) and removed the need for animals to consume imported feedstuffs whose production might otherwise drive deforestation and land conversion elsewhere in the world. However, it appears that for them and their peers protein crops such as legumes remain primarily a component of attempts to satisfy sub-Saharan Africa’s appetite for protein through the intensification of small-scale livestock production, rather than forming the basis of any distinctive investor vision or programme of investment. While the cultivation of these crops might serve as a means of increasing the sustainability of animal proteins (and of smallholder arable agriculture), they were not perceived to provide a distinct environmental or dietary solution in their own right.

Footnotes

4 No similar analysis of the likely geographical location of the animal protein enterprises financed by the other two investor networks could be undertaken. This is because sub-Saharan Africa’s meat, dairy and animal feed sector is far larger, more fragmented and more geographically dispersed than its incipient alternative protein industry. As a result, the availability of data on animal protein enterprises in sub-Saharan Africa is far more variable. As such, no single database of privately owned animal protein companies exists and constructing such a database was beyond the scope of this research.

Post a new comment »